Why K-Beauty Is Dominating Amazon Right Now (2026)

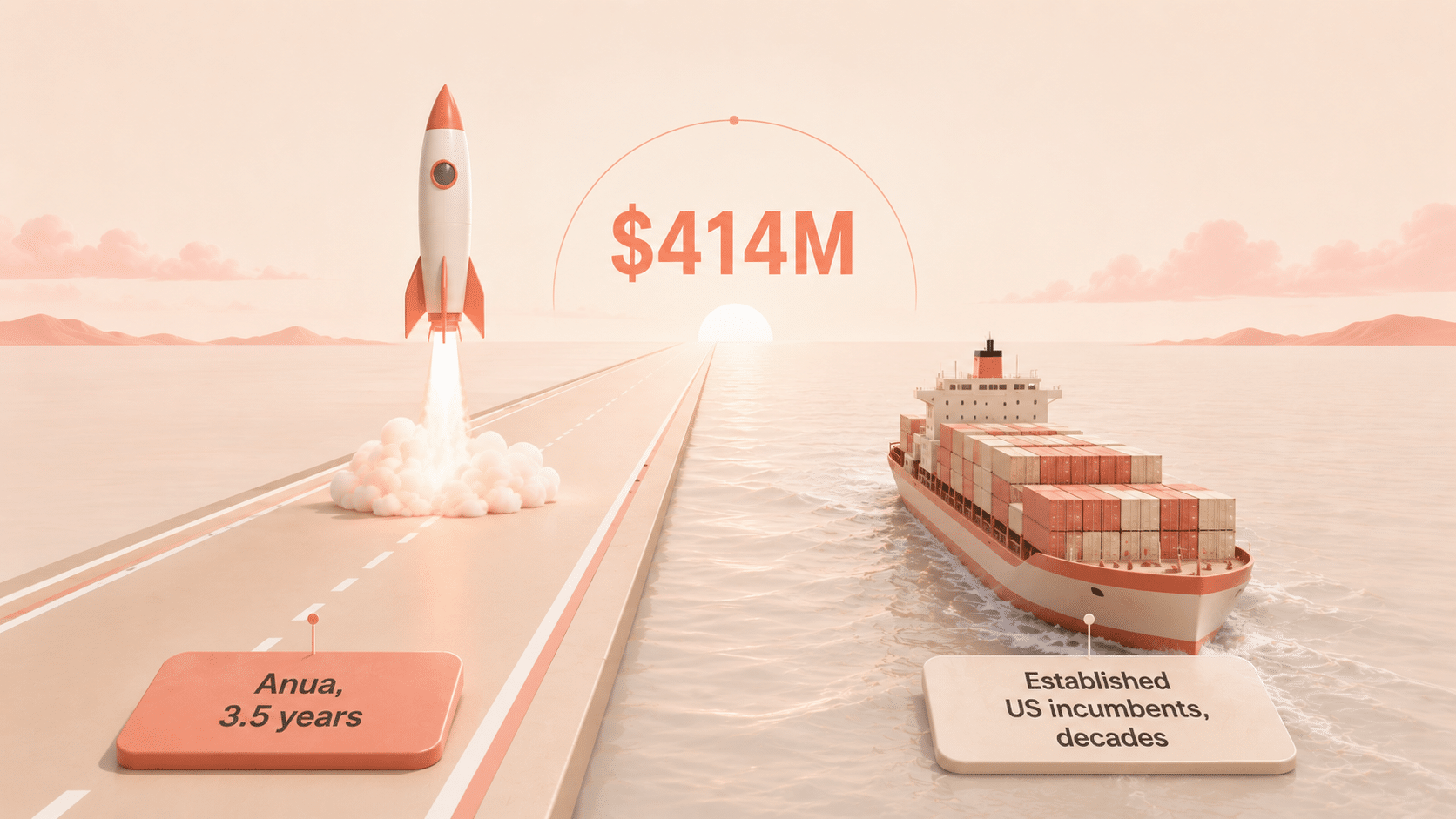

A Korean skincare brand called Anua launched on US Amazon in late 2022. Three and a half years later it shows up on SellerSnooper's top-seller leaderboard at roughly $414 million in trailing twelve-month revenue — climbing while a 15% tariff and the end of duty-free shipping push against it.

To understand how a cohort of foreign brands is out-earning decades-old American incumbents on their own platform, you have to start with what K-beauty actually is.

What Is K-Beauty, Exactly?

K-beauty is shorthand for Korean skincare — a category built less on a single look than on a philosophy: skin first, makeup second. Where Western beauty spent forty years selling outcomes (“glowing,” “youthful,” “confident”), K-beauty sells steps and ingredients. The aesthetic goal everyone now recognizes from TikTok is “glass skin”: a clear, dewy, almost reflective complexion achieved through layering rather than coverage.

That distinction matters commercially, because it changes what the shopper is buying. A K-beauty customer isn't buying a promise. They're buying a specific compound with a specific job — and that's where the category's durability comes from.

The Ingredients Doing the Heavy Lifting

Four hero ingredients anchor most of K-beauty's biggest Amazon sellers, and each one is verifiable in a way marketing copy isn't.

Heartleaf

Houttuynia cordata — a soothing, anti-inflammatory botanical, and the compound Anua built its entire identity around. It's the cleanest example of a Korean brand owning an ingredient from a near-zero starting point in the US market.

Snail Mucin

The ingredient that arguably broke K-beauty into the US mainstream. As dermatologists explain, snail mucin works primarily on hydration and protecting the skin barrier. It's the backbone of COSRX's best-known products, and the search data shows it: on the brandless term “snail mucin,” COSRX's Repairing Serum leads with about 46% of clicks and 49% of conversions (2026), per Amazon's Brand Analytics Top Search Terms report. The brands trailing it are mostly generic imitators — a sign of how completely COSRX owns the ingredient.

Rice

Korean brands have drawn on rice's centuries-long place in domestic skincare — rice water, rice bran extract, rice ceramides — and turned it into a category they own outright on Amazon. On the brandless “rice toner” search, all three top-clicked brands are Korean (I'm From, Anua, and either Haruharu or TIRTIR depending on the period), with I'm From's Rice Toner taking 33–64% of clicks across the two years.

The same pattern holds on “rice serum,” “rice water toner,” and “rice milk toner” — Korean top three on every one. On the branded search “anua rice toner,” Anua's Rice 70 Glow Milky Toner converts at 76–80%.

PDRN

The newest and the most clinically loaded of the four. It stands for polydeoxyribonucleotide, and as skincare and dermatology sources describe it, it's made of purified DNA fragments (usually derived from salmon or trout) that share roughly 98% similarity with human DNA, which is what makes it biocompatible.

Where snail mucin hydrates, PDRN is focused on recovery and repair. Crucially, it isn't a fad ingredient invented for a campaign: it had been used in medical settings for wound healing and skin regeneration for decades before it ever reached a serum.

A shopper who Googles “heartleaf,” “rice toner,” or “PDRN” finds substance. A shopper who Googles “glowing youthful skin” finds ad copy. Verification is the difference.

How K-Beauty Got Here: From Sheet Masks to the “Second Wave”

K-beauty isn't new to America. Its first wave in the 2010s was about novelty: sheet masks, BB creams, ten-step routines that made for good magazine features. What's happening now is different enough that the industry calls it the second wave: ingredient-led, TikTok-native, and far bigger.

You can watch the pipeline work in real time with PDRN. The ingredient first went viral as an in-clinic injectable — the “salmon DNA facial” — after celebrities including Kim Kardashian and Jennifer Aniston drew global attention to it, and brands raced to bottle a topical, needle-free version for the mass market. Snail mucin made the same journey a few years earlier.

COSRX is a useful timeline marker. Founded in Seoul in 2013, it's now sold in more than 120 countries — a decade-long climb that maps almost exactly onto K-beauty's rise in the US.

Why Shoppers Can't Get Enough

Demand this strong usually has more than one driver, and K-beauty has three stacked on top of each other:

- Verification culture. Outcome claims used to work because shoppers had no way to check them before buying. Now verification takes thirty seconds — a TikTok before-and-after, a 200-comment Reddit ingredient breakdown, a clinical-study summary on Google. Ingredient claims survive that scrutiny; vague outcome claims don't.

- Value. K-beauty consistently lands in a sweet spot most US brands can't reach: prestige-level formulation at mid-tier prices (more on why in a moment).

- Where the shopping happens. According to NielsenIQ, 70% of K-beauty sales now happen online, with TikTok Shop functioning as a powerful launchpad that feeds brands like Anua and Medicube straight into Amazon, Sephora, and Ulta. Discovery and the purchase live on the same phone.

The Manufacturing Secret Behind the Price Tags

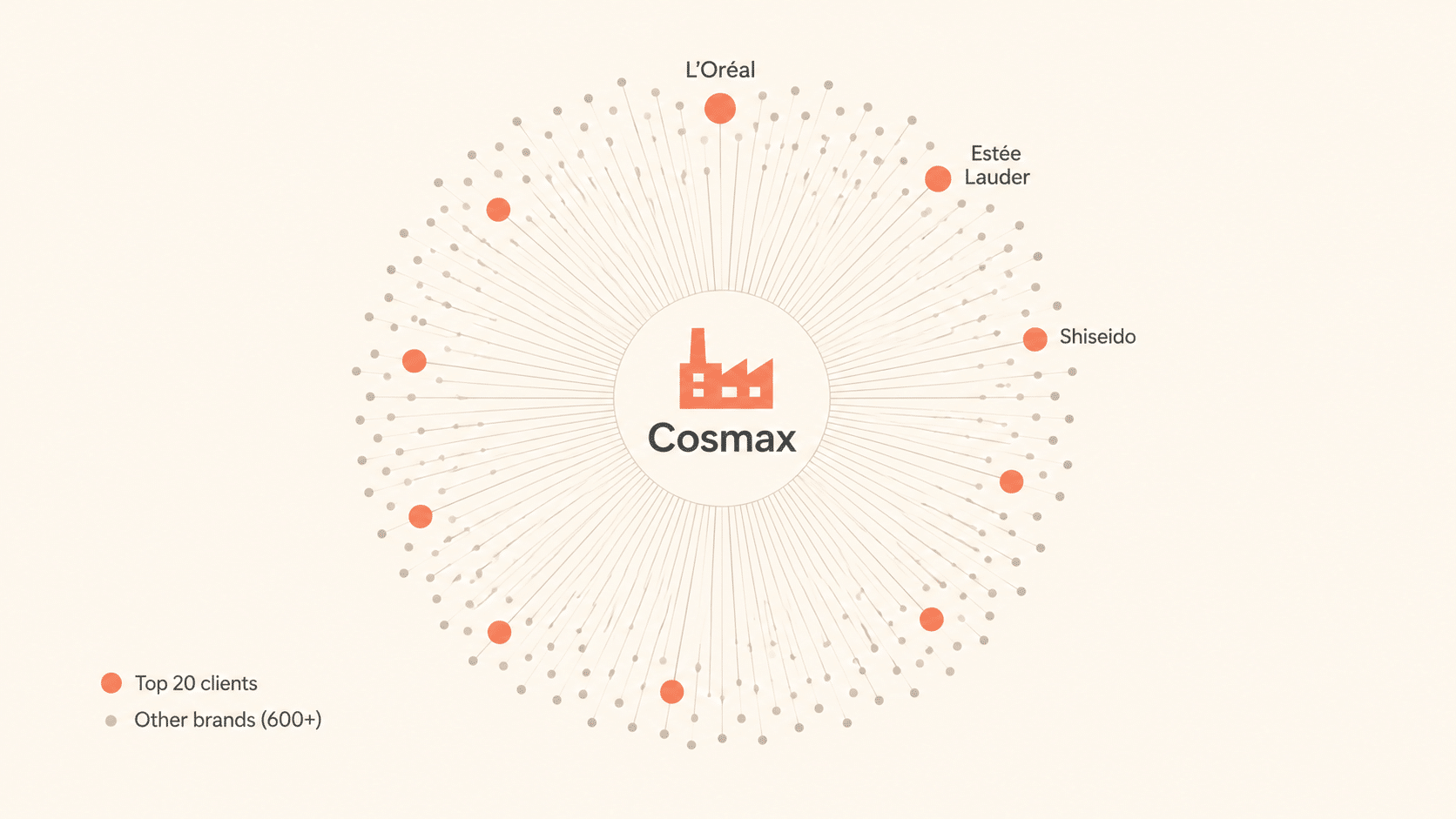

The value question has a concrete answer, and it sits in South Korea's manufacturing base. The country hosts the most concentrated cosmetic ODM/OEM ecosystem in the world — companies that handle research, formulation, and production so a brand can focus on marketing.

The scale is hard to overstate. Cosmax alone manufactures for more than 600 brands worldwide, and 15 of the 20 largest global cosmetics companies — including L'Oréal — entrust their manufacturing to it. It was, in fact, the first Korean ODM to land an L'Oréal contract.

What that means for a new Korean brand is access to clinical-grade formulation and scaled production at a cost structure most US founders building from scratch simply can't match.

So, Korean brands routinely hit prestige-quality formulas at mid-tier price points, while a US brand trying to match that quality from the ground up tends to land far higher.

How Big Is the K-Beauty Market Now?

Big enough that “trend” no longer describes it.

- Globally: Korea's cosmetics exports hit a record $11.4 billion in 2025, up 12.3% year over year, with basic skincare alone accounting for $8.54 billion (Ministry of Food and Drug Safety).

- In the US: NielsenIQ reported K-beauty sales on track to top $2 billion in 2025 — up more than 37% year over year, several times the broader beauty market's single-digit growth.

- The pace of growth: In 2024 the figure hadn't yet cracked $1 billion. The category roughly doubled in a year.

- Position: Korea has now overtaken France as the leading cosmetics exporter to the US.

What the Search Data Actually Shows

Market totals tell you the category is big. Amazon's own search data tells you how the brands win — and it's more aggressive than the revenue numbers suggest. The figures below come from Amazon Brand Analytics' Top Search Terms report, which lists the three most-clicked brands for any given search along with their click and conversion share.

One note for fair reading: Amazon removed bot traffic from this report starting Week 14, 2026, which trimmed reported volume on some high-traffic generic terms even as real demand grew.

The dominance plays out in three layers:

Layer 1 — The generic category terms

On “korean skincare” (2026, search-frequency rank ~16,900), the three most-clicked brands — medicube, Anua, and JiYu — are all Korean. The same holds for “k beauty” and “korean beauty.” Not one legacy US brand cracks the top three on any of them. The category's most valuable front door belongs entirely to the cohort.

Layer 2 — The brandless ingredient terms

This is where the mechanism gets interesting, because the dominance extends to brandless ingredient terms — searches with no brand name in them at all:

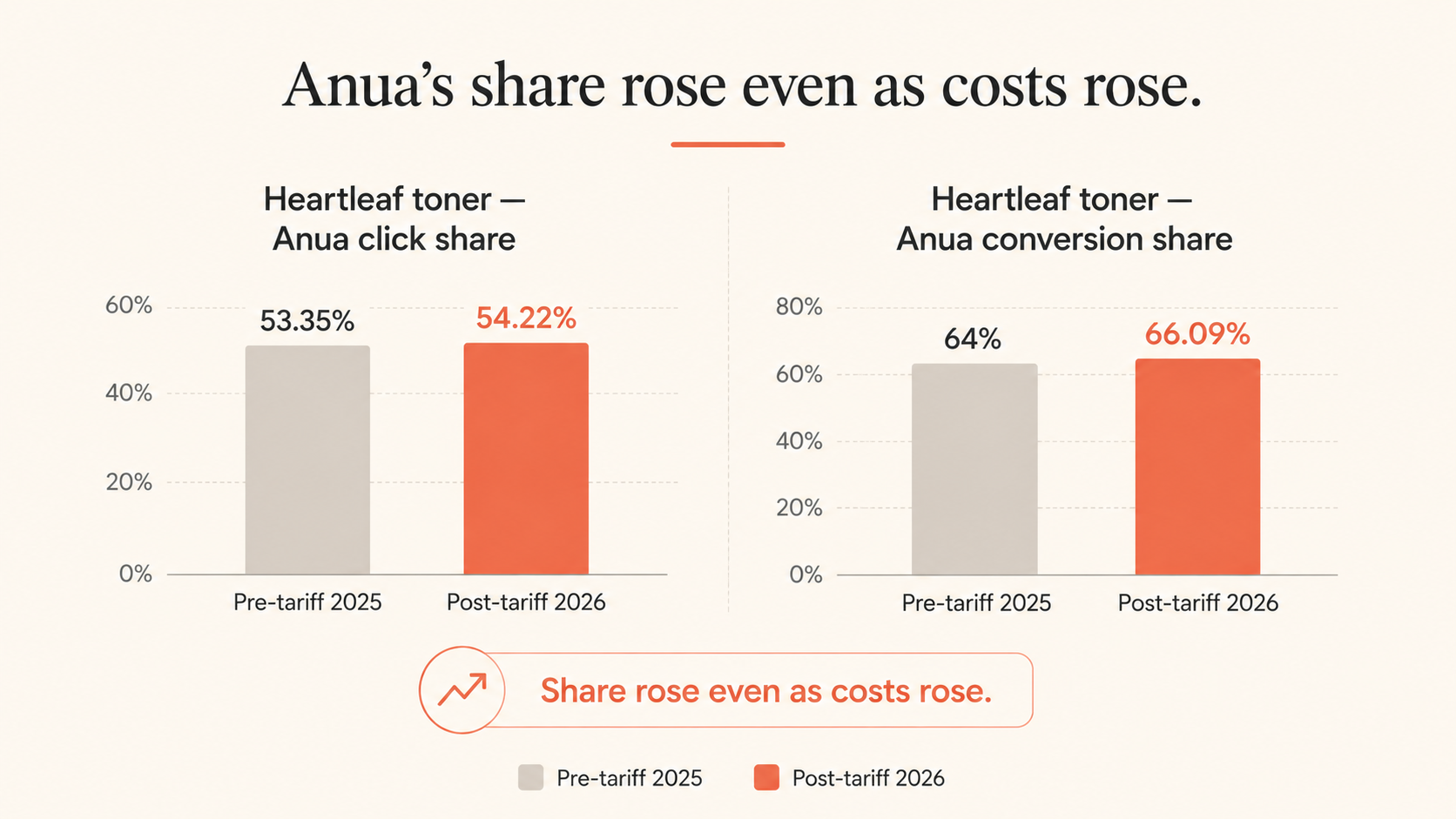

- “heartleaf toner” — Anua's Heartleaf 77 Soothing Toner takes 54.22% of clicks and 66.09% of conversions (2026). The next two brands (JMsolution, numbuzin) are also Korean.

- “snail mucin” — COSRX leads with about 46% click and 49% conversion share.

- “rice toner” — I'm From, Anua, and a third Korean brand take the top three; Korean brands win every rice-anchored ingredient search.

- “pdrn” — top three are again all Korean (VT Cosmetics, medicube, Anua).

Layer 3 — The branded terms

On branded searches, conversion gets close to total:

- “anua heartleaf toner” — Anua converts at 75.52% click / 81.69% conversion (2026).

- “anua heartleaf 77 soothing toner” — climbs to 81.6% / 83.74%.

Conversion that high means the shopper didn't arrive to compare — they arrived to buy, having already decided somewhere else (usually TikTok). Put the three layers together and the mechanism becomes visible: TikTok creates the branded intent, the branded intent trains Amazon's algorithm, and the algorithm then hands the cohort the generic and ingredient searches too. By the time a competitor notices, the position has been compounding for months.

Where K-Beauty Doesn't Win

For accuracy's sake — and because the limits of the pattern are as instructive as the dominance — it's worth naming where K-beauty has not colonized the search results. Two ingredients stand out:

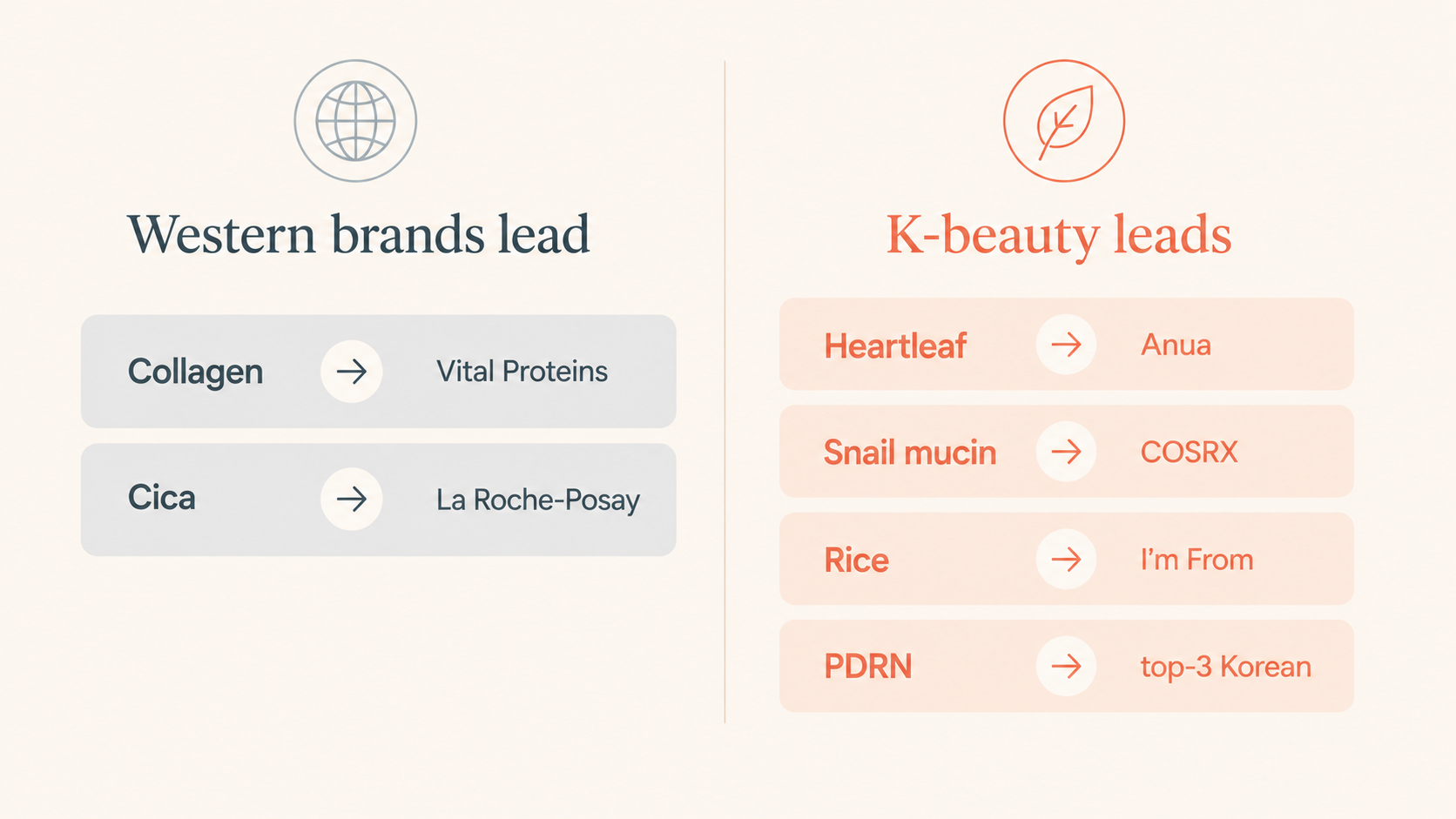

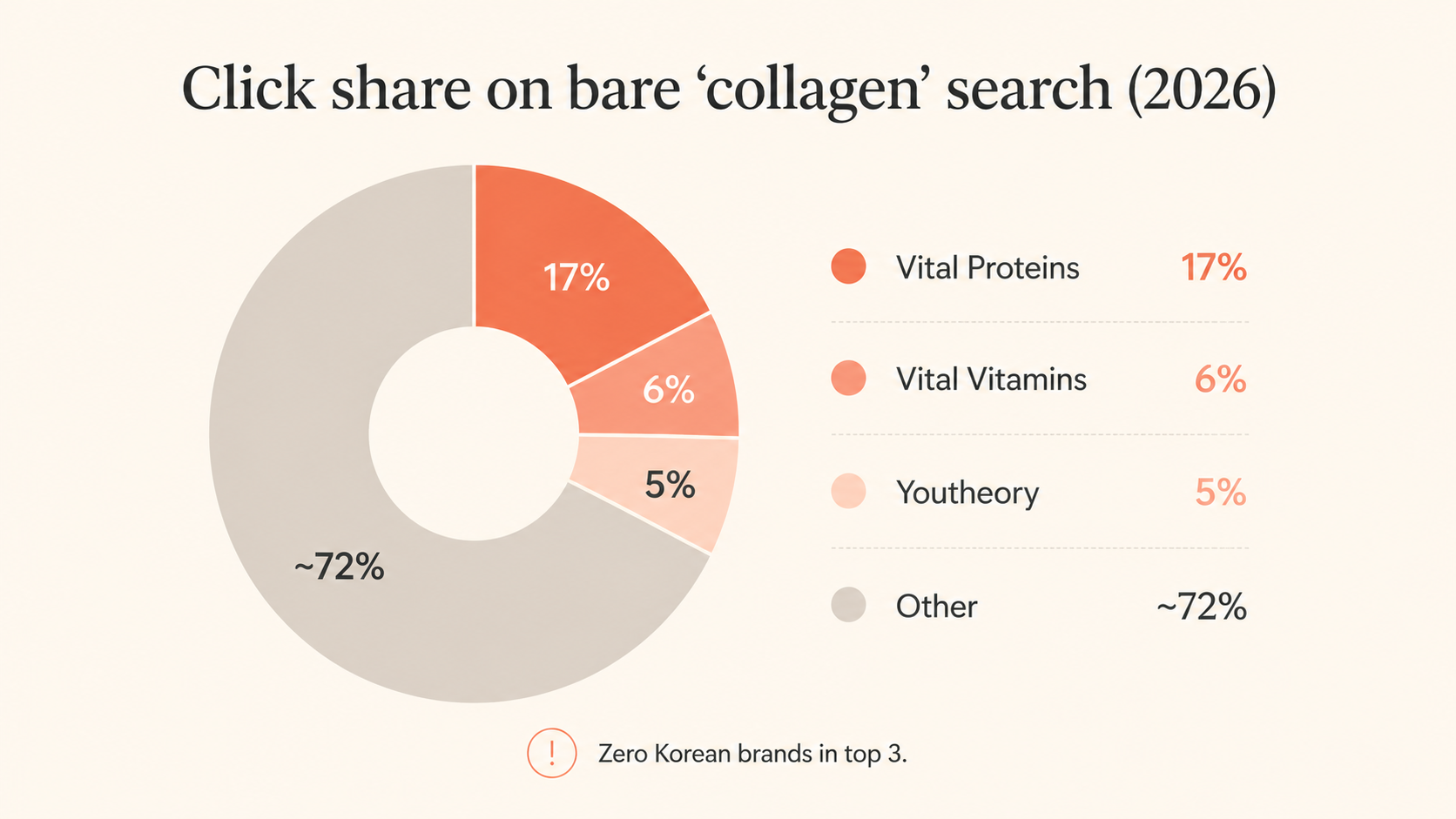

Collagen

On the bare term “collagen” (a top-300 search by frequency, higher volume than any K-beauty ingredient term) the three most-clicked brands are Vital Proteins, Youtheory, and Vital Vitamins. All American. All ingestible supplements.

The same pattern repeats across “collagen peptides,” “collagen powder,” “collagen gummies,” “marine collagen,” “multi collagen,” and “hydrolyzed collagen”: Western supplement incumbents lock down the top three. On the topical side it's slightly more mixed but still not a K-beauty win, “collagen serum,” “collagen face cream,” and “collagen cream” are led by L'Oréal Paris, with medicube and SUNGBOON Editor trailing in #2 or #3.

Korean brands do win exactly one niche inside the ingredient: collagen masks. BIODANCE's Bio-Collagen Real Deep Mask takes 37–42% of clicks on “collagen face mask” and “collagen mask.” But that's a sub-segment, not the ingredient.

Cica (centella asiatica)

K-beauty is closely associated with cica products, but on the bare term “cica,” La Roche-Posay's Cicaplast Balm B5 takes roughly 19–21% of clicks across both years, more than any single Korean brand.

VT Cosmetics and Dr.Jart+ trail in #2 and #3. Korean brands dominate when the search is qualified — on “centella probio-cica,” SKIN1004 takes more than half the clicks — but the bare ingredient belongs to a French pharmacy brand.

Read together, collagen and cica sharpen what's actually happening. K-beauty wins ingredient searches when the cohort either got there first on a novel compound (heartleaf, PDRN), successfully reframed a clinical ingredient as topical skincare (snail mucin, PDRN), or branded a botanical the West hadn't claimed (rice).

It has not displaced ingredients with decades-deep Western incumbency — and probably won't on collagen as long as the category is anchored by ingestible supplements. Which is exactly why positioning early on the next compound matters as much as it does.

How Big Is K-Beauty on Amazon Specifically?

The leaderboard reflects all of the above. Anua's roughly $414 million puts it among the very top D2C earners on SellerSnooper's May 2026 board, with COSRX and the broader Korean-origin cohort close behind. (These are live snapshots that move month to month — Anua's own 30-day growth reading was sitting above 90% at last check — so any figure you cite should carry a date.)

The demand pipeline behind it is just as lopsided: K-beauty is the top-selling beauty category on TikTok Shop, with sales up 132% in 2025.

The Tariff Headwind — and Why Growth Didn't Stop

Here's what makes the 2026 picture genuinely strange. K-beauty is growing through a real cost shock.

- The 15% reciprocal tariff on Korean imports took effect around August 1, 2025.

- The de minimis exemption — which had let shipments under $800 enter duty-free — ended on August 29, 2025.

- The exposure was significant: the US had imported an estimated $1.7 billion in Korean cosmetics in 2024, per the US International Trade Commission.

Costs went up. The brands grew anyway — so, how?

From 2025 to 2026, Anua's grip on the brandless “heartleaf toner” search actually tightened: from 53.35% clicks and 64% conversions in 2025 to 54.22% and 66.09% in 2026, even as the term's overall search volume rose.

Demand that sticky absorbs a price increase. It also helps that brands operating through US-registered entities weathered the change far better than those relying on direct-to-consumer shipping from Korea.

Where the Next Wave Is Forming

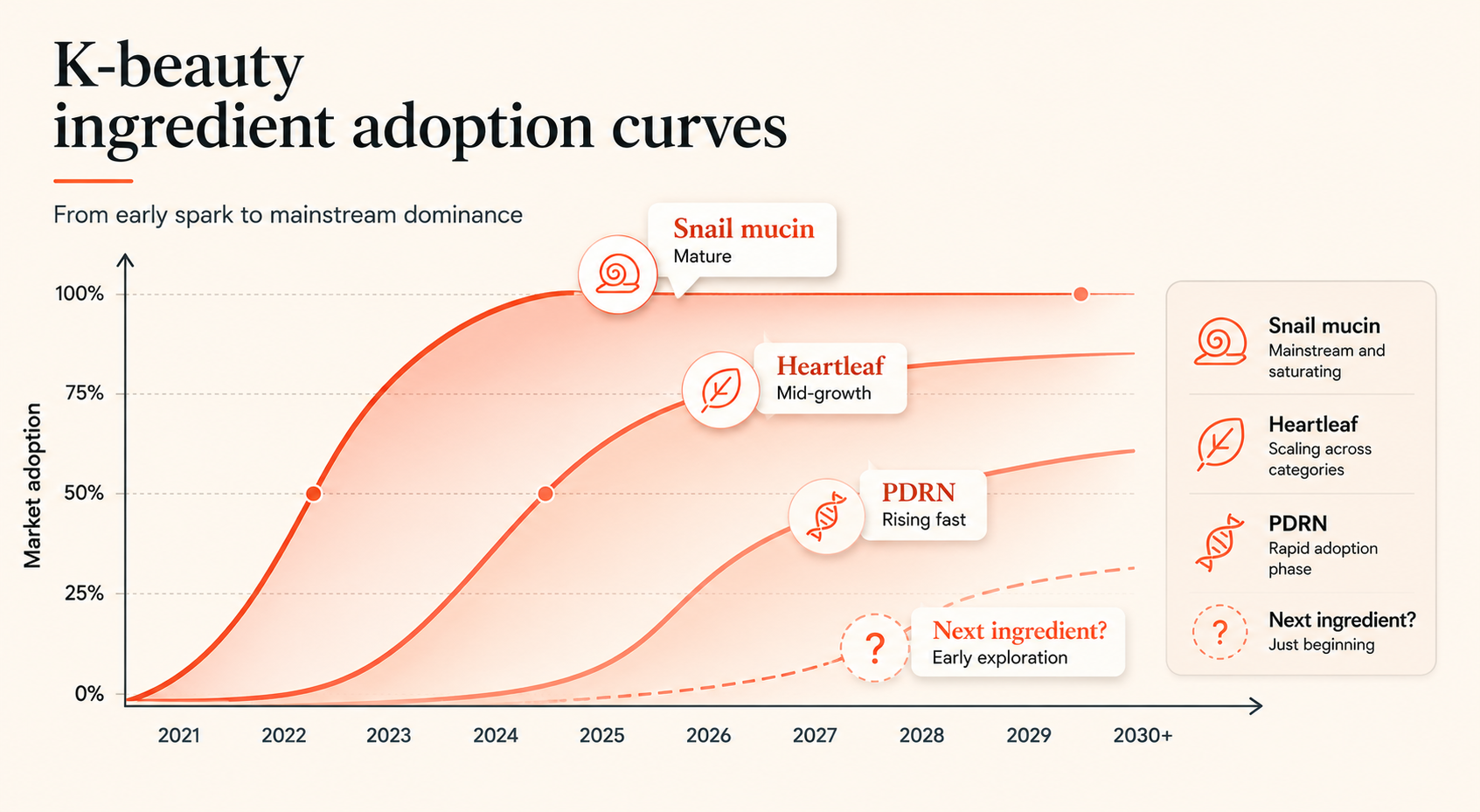

If snail mucin was the last ingredient to make the leap from clinic to cart, PDRN is the next one mid-jump — what the industry calls the “medicosmetic pivot.”

And the search data suggests it has already arrived: “pdrn” now ranks around 5,100 in search frequency — on par with the most-searched snail-mucin terms, remarkable for an ingredient that was still niche a year ago. Every top-clicked brand on it is Korean.

The brands positioned at the front of that wave are, not coincidentally, the same ones near the top of the revenue board. Medicube's parent company APR saw sales rise 218%, powered largely by PDRN-anchored products. The brands tracking just below the headline revenue tier — Medicube, BIODANCE, Dr. Althea — are the ones worth watching for the next breakout.

The flip side worth naming: the same data that shows dominance also shows saturation.

On snail mucin and heartleaf, generic copycats now crowd the second and third spots. The originator still wins, but the moat narrows as the ingredient ages. That's exactly why getting in early on the next compound matters so much — and exactly the dynamic the collagen and cica examples expose.

So, What Does This Mean?

K-beauty hasn't won a trend on Amazon; it's won a category, and it did so with a repeatable system rather than a marketing budget:

- Ingredient credibility brings shoppers who verify before they buy.

- A world-class manufacturing base delivers prestige formulas at accessible prices.

- TikTok pre-warms the traffic, and Amazon's algorithm — fed by conversion data the search reports lay bare — rewards the conversion that follows.

- Even tariffs designed to slow it down haven't.

For US brands and sellers, that's an uncomfortable position — but a legible one. The cohort's moves are visible, sequential, and learnable. How to run them is its own subject, and the one we'll break down next.

Frequently Asked Questions

Why is K-beauty so popular on Amazon right now?

Three forces stack together: TikTok-driven demand, ingredient-led marketing that shoppers can verify before buying, and a Korean manufacturing base that delivers prestige-grade formulas at mid-tier prices. The result is fast growth — US K-beauty sales reached about $2 billion in 2025, up more than 37% year over year.

What is “glass skin”?

Glass skin is the K-beauty aesthetic goal of a clear, smooth, intensely hydrated complexion that looks almost reflective — like glass. It's achieved through layering hydrating steps rather than heavy makeup coverage.

What are the main K-beauty ingredients?

The four anchoring most top Amazon sellers are heartleaf (a soothing, anti-inflammatory botanical), snail mucin (for hydration and barrier support), rice (for hydration and brightening, with deep roots in Korean skincare tradition), and PDRN (for skin repair and regeneration).

What is PDRN in skincare?

PDRN stands for polydeoxyribonucleotide — purified DNA fragments, usually derived from salmon or trout, that are about 98% similar to human DNA. It was used in medical settings for wound healing for decades before becoming a viral topical skincare ingredient focused on repair and regeneration.

Did tariffs hurt K-beauty sales in the US?

They raised costs: a 15% tariff on Korean imports took effect around August 1, 2025, and the duty-free de minimis exemption ended August 29. But demand proved strong enough to absorb the increase, and the category kept growing — brands operating through US-registered entities weathered it best.

Which Korean brands dominate Amazon?

Anua leads, at roughly $414 million in trailing twelve-month revenue, with COSRX and Medicube close behind. Amazon's own search data shows them topping not just their branded searches but generic terms like “korean skincare” and brandless ingredient terms like “heartleaf toner,” “rice toner,” and “snail mucin.”